Translated using ChatGPT service.

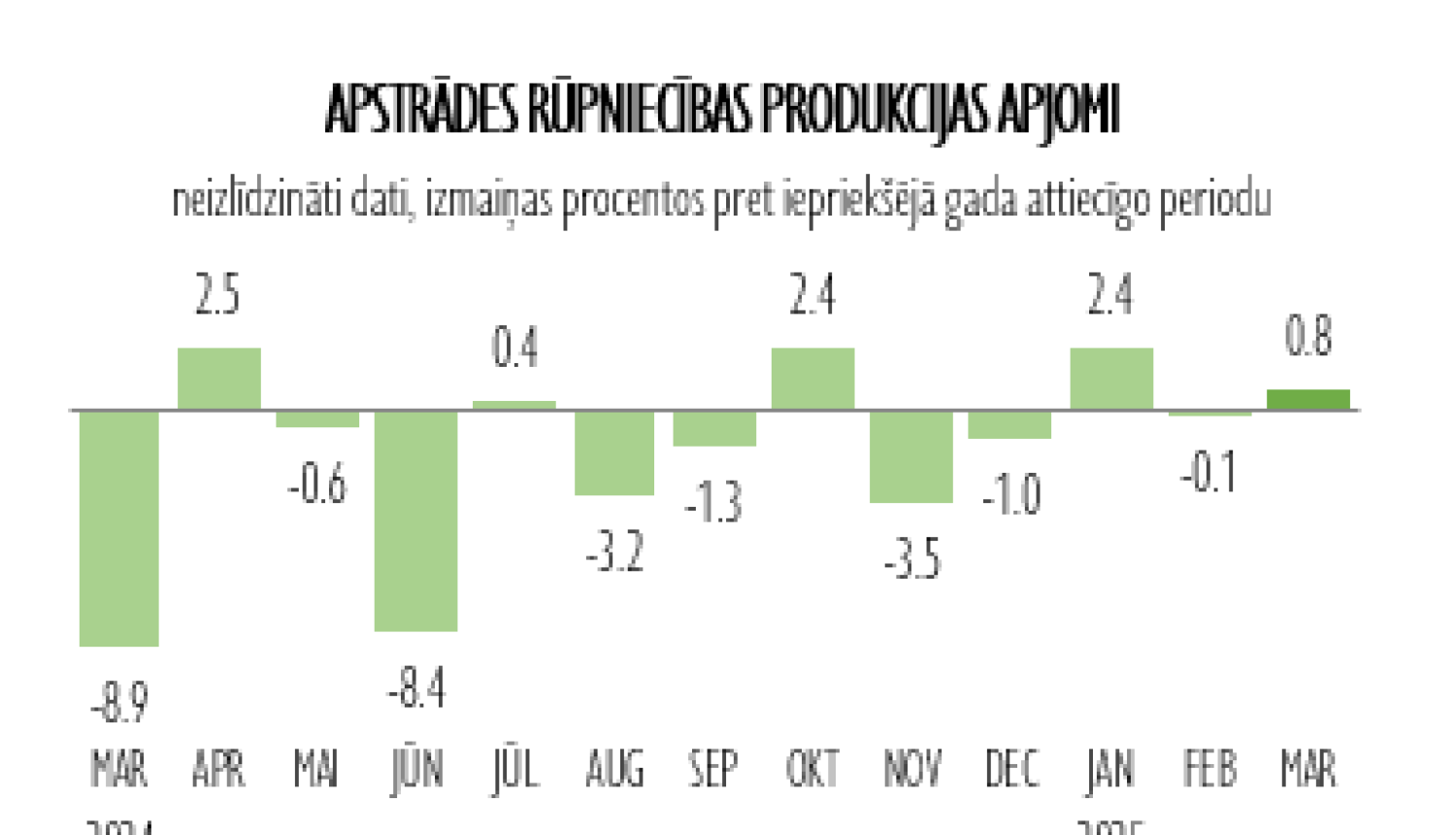

According to data from the Central Statistical Bureau, the output of the manufacturing industry in March 2025, compared to March 2024, increased by 0.8% in unadjusted data, but decreased by 1.7% in calendar-adjusted data. Overall, in the first three months of the year, manufacturing production volumes were 1% higher than in the corresponding period of the previous year (according to unadjusted data).

There are still differing development trends in the sub-sectors of the industry. In March of this year, compared to the same month of the previous year, the most significant positive impact on manufacturing came from wood processing (+9.2%), food production (+9.3%), and the production of non-metallic mineral products (+22.7%). The production of automobiles, trailers, and semi-trailers (+10%), printing and recorded media reproduction (+11.3%), and the production of fabricated metal products (+3.2%) also increased. On the other hand, the production volumes of the chemical industry (-9%) and computers, electronic and optical equipment (-6.7%) significantly decreased.

In March, the turnover of the manufacturing industry in current prices increased by 7.9% year-on-year, driven by an increase in both the volume of products sold in the domestic market and exports – up by 9.5% and 7%, respectively. The most significant increases were observed in the sales of wood processing, food products, and non-metallic mineral products.

It is expected that in 2025, the manufacturing industry will maintain positive growth trends on a monthly basis. This will continue to be driven by the recovery of demand in external markets and an increase in export volumes. However, challenges will remain for companies whose activities are still closely linked to the markets of Russia and other CIS countries – these companies will need to continue restructuring their cooperation directions, seeking new supply and sales markets. Meanwhile, industries focused on the domestic market will be significantly influenced by household purchasing power dynamics, which could gradually improve in the coming months due to wage increases, tax changes, and price stabilization.

At the same time, industrial development could be hindered by external risks, including potential new import tariffs in the US market, which could affect the competitiveness of Latvian exporting companies. Overall, while forecasts are cautiously positive, the industry will need to maintain flexibility and the ability to adapt to changing global trade conditions.